Regain control of your cash flow

Money is as vital to business as oxygen is to a human being and just as no one pays attention to the air they breathe until it runs out, many entrepreneurs don't worry about their cash flow until it becomes scarce and a matter of survival.

The fragility of the financial health of the self-employed, VSEs and SMEs was revealed during the health crisis when several studies, including one by the National Bank of Belgium, published in June 2021 and entitled "Belgian corporate sector liquidity and solvency in the COVID-19 crisis: a post-first-wave assessment", highlighted the weakness of their liquidity, which only allowed them to "hold out" for an average of some two months.

The good news is that this is not a foregone conclusion, but before talking about solutions, it is important to determine the main causes of a fragile cash flow.

Understanding the causes of cash flow problems

This is generally explained by:

- Confusion between cash flow and profit. Paradoxically, companies do not go bankrupt because they are not profitable enough but rather because of a lack of cash flow. In this regard, the law speaks of persistent cessation of payment and loss of creditworthiness;

- Undercapitalisation of the company and insufficient working capital, i.e. equity and long-term capital;

- Inadequate means of finance. Long-term investments are financed by short-term loans;

- A fall in business that is not offset by a reduction in expenses, often characterised by overcapacity and high fixed costs;

- An "uncontrolled" increase in business;

- A structural decline in profitability negatively impacting the self-financing capacity;

- Customers who are "bad payers" or who "default";

- Poor management of working capital requirements, which are mainly comprised of receivables due within one year, inventories and suppliers.

How can these cash flow problems be solved?

Anticipation is the key word.

It's always dangerous to lose your perspective, but in times of crisis it can be catastrophic.

Make it a point to monitor your results monthly, update your financial plan, use a cash flow statement and, above all, implement a cash flow monitoring statement, an indispensable tool that you can use to anticipate the health of your cash flow.

Learn how to read a balance sheet and income statement, this will help you enormously in understanding financial flows. Ask your accountant, they will be happy that someone is interested in what they do.

In order to improve your cash flow, increase your permanent capital (equity and long-term debt) and reduce your working capital requirements, which you need to run your operating cycle from purchasing raw materials to paying your customers.

What can you do to increase your revenue and decrease your cash outflow?

Here are some practical avenues you can explore:

- Increase your self-financing capacity by improving the profitability of your sales.

- Reduce the average debt recovery time through a strict procedure from assessing the creditworthiness of your customers, using credit limits and issuing your invoices as soon as possible to factoring which may be an option to consider although it has a cost.

- Obtain other sources of funding such as bank/partner loans, capital increase and other alternative financing (public aid, crowdfunding, etc.)

- Selling unproductive and/or unnecessary assets can also help you generate cash.

On the other hand, in order to reduce and/or slow down cash outflow, you will need to negotiate longer payment terms with your suppliers, reduce your expenses and optimise your stock levels through the rigorous management of rotations, security levels, etc.

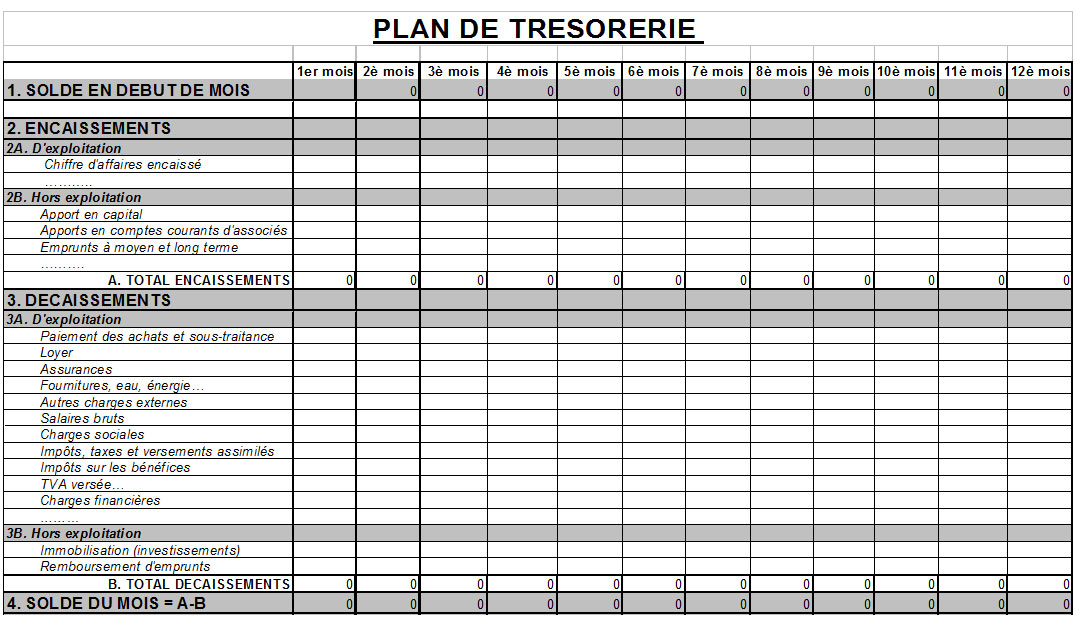

The cash flow monitoring statement

The cash flow monitoring statement is a key part of your cash flow improvement plan. This indispensable tool will help you to

- Anticipate cash flow surpluses and/or deficits;

- Determine how long your balance will remain in debit or credit and the amount;

- Decide whether to invest surpluses or finance deficits and over what period of time;

- See revenue, cash outflow and the resulting cash in hand on a timeline;

- Estimate short-term cash flow requirements;

- Take corrective action.

In order to prepare this statement, you will need the forecasted inflows mainly comprised of expected customer payments, possible loans (banks, shareholders, etc.) and other inflows (possible rents, dividends, etc.) and the forecasted outflows comprised of suppliers to be paid, salaries and wages, corporate tax, VAT and other outflows such as debt repayment.

As far as revenues are concerned, the better your overview of your customers' payment behaviour and the potential seasonal nature of your activities, the more accurately you will be able to forecast future receipts.

Cash outflows are, by nature, more controllable provided your accounting is up to date. If your cash flow is strained, you can decide what priorities to give with regard to any late payment penalties.

In practical terms, this statement will start with the cash position at a point in time, for example 1 January 2022, and take into account all expected revenue and cash outflows over the following weeks. Customer and supplier schedules will be very useful for building your cash flow statement.

| A golden rule: the greater pressure your cash flow is under, the tighter your control will be. In a crisis situation, it is not unusual for the cash flow statement to be updated on a daily basis. |

It's a lot of work, but with this approach, you won't lose your perspective and you will no longer suffer events. Taking control of your cash flow will give you the anticipation you need to take the necessary measures as soon as possible and with complete peace of mind.

If you don't take care of your cash flow, your cash flow will take care of you. So prevention is better than cure.